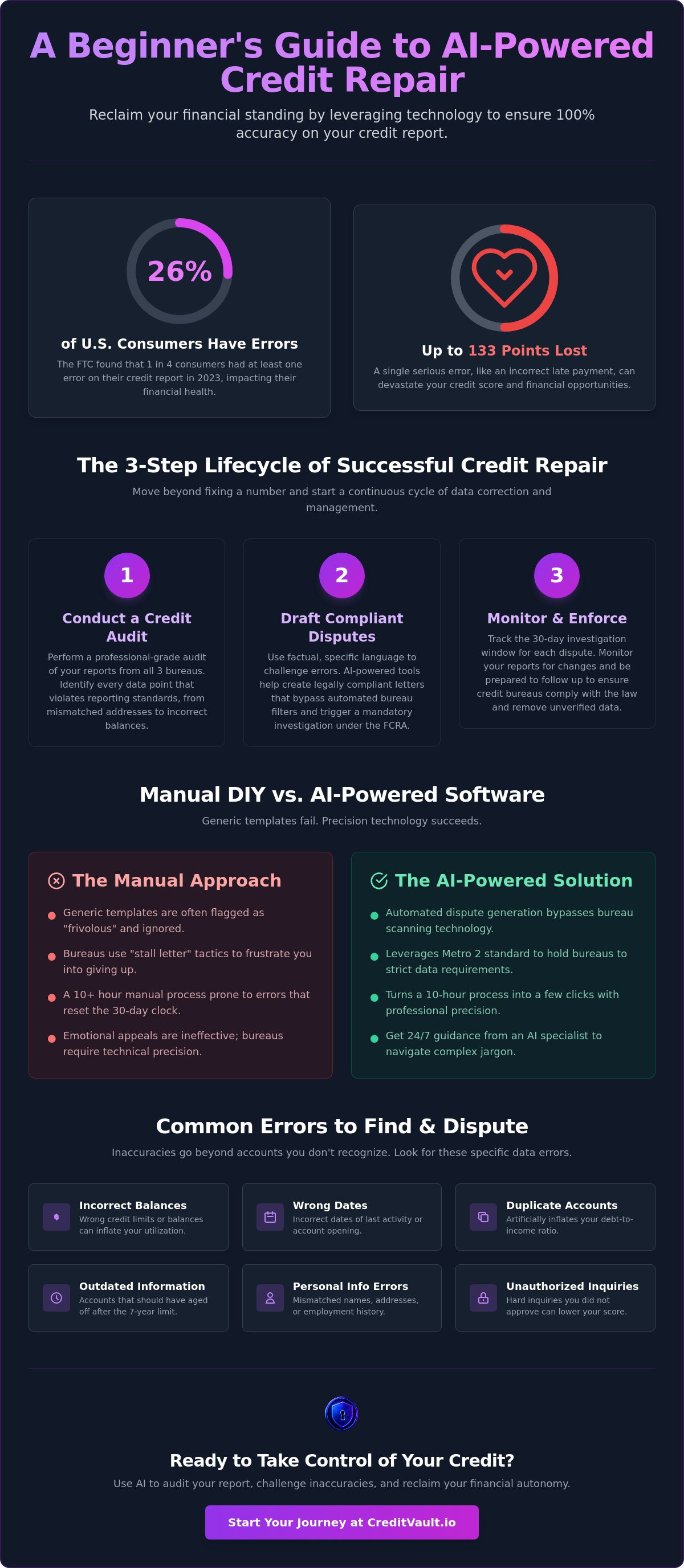

According to the FTC, 26% of U.S. consumers found at least one error on their credit reports in 2023. It's a sobering reality that your financial health often depends on data you didn't even input. You've likely felt the weight of this system; the confusion over credit bureau jargon and the fear that a single mistake could make your situation worse are common hurdles. This guide to credit repair for beginners is designed to remove that friction and replace it with active participation.

You'll master the fundamentals of credit repair and learn how to use AI technology to challenge inaccuracies with professional-grade precision. We'll show you how to navigate the 2026 regulatory landscape, including the updated Fair Credit Reporting Act standards that now require stricter verification from bureaus. This article provides a clear roadmap to a better score. You'll discover how automated tools can handle the heavy lifting, ensuring your data is reported accurately while you reclaim your financial autonomy.

Key Takeaways

- Reclaim your standing by exercising your legal right to challenge inaccurate data under the Fair Credit Reporting Act.

- Simplify credit repair for beginners by moving beyond the score and identifying specific reporting errors through a deep data audit.

- Scale your efforts by using AI to automate dispute letter generation, turning a 10-hour manual process into a few clicks.

- Leverage the Metro 2 standard to hold bureaus accountable to the industry's most rigorous data-reporting requirements.

- Get 24/7 guidance from an AI Credit Specialist (Mo) to navigate complex bureau jargon and ensure your disputes are handled with precision.

What Is Credit Repair and How Does It Work for Beginners?

Real credit repair isn't a secret loophole or a magic delete button. It's the systematic process of auditing your financial data and exercising your legal right to challenge any information that's inaccurate, outdated, or unverifiable. According to the FTC, 26% of U.S. consumers found at least one error on their credit reports in 2023. For many, the journey into credit repair for beginners starts with the realization that credit bureaus are not infallible. They are private companies that profit from your data, and they frequently get the details wrong. A single serious error, such as a payment reported 90 days late when you were never delinquent, can reduce your credit score by up to 133 points.

It's vital to understand that you aren't trying to "delete the truth." You are enforcing a 100% accuracy mandate. If a bank reports a late payment but cannot provide the documentation to prove it happened on that specific date, that data is unverifiable. Under federal law, unverifiable data cannot remain on your report. Starting your journey with a technology-first approach allows you to detect these technicalities before they become permanent stains on your financial record.

The Legal Foundation: Your Rights Under the FCRA

The Fair Credit Reporting Act (FCRA) serves as your primary legal shield. It dictates that credit bureaus must investigate any disputed item within 30 days. If they fail to verify the information within this window, the law requires its immediate removal. This protection is bolstered by the Credit Repair Organizations Act (CROA), which regulates how professional services can assist you in this process. An "inaccurate" item includes more than just accounts that don't belong to you. It covers specific data points like:

- Incorrect account balances or credit limits that increase your utilization.

- Wrong dates for account openings or the date of last activity.

- Duplicate accounts that artificially inflate your debt-to-income ratio.

- Accounts that should have aged off the report after the legal seven-year limit.

Why Traditional "Fix My Credit" Methods Often Fail

Have you ever sent a dispute letter only to receive a generic response claiming your request was "suspicious"? This is the "stall letter" tactic bureaus use to frustrate you into giving up. Many people start their credit repair for beginners journey by downloading a generic dispute template. This is often a mistake. Credit bureaus use sophisticated scanning technology to identify these templates and flag them as "frivolous." When a dispute is marked frivolous, the bureau can legally refuse to investigate it. Additionally, manual errors in your letters, such as a missing account number or a typo in your address, can reset the 30-day investigation clock. By using AI-driven tools, such as those offered by CreditVault.io, you bypass these manual pitfalls and communicate with bureaus in a language they are legally obligated to respect.

The 3-Step Lifecycle of Successful Credit Repair

Successful credit repair for beginners requires a shift in mindset. You aren't just "fixing" a number; you're managing a continuous cycle of data correction. This isn't a one-time event where you mail a letter and wait for a miracle. It's a marathon of precision and persistence. If you treat it like a technical audit rather than an emotional appeal, you'll see better results. The process is a loop of identifying errors, challenging them with evidence, and monitoring the outcome to ensure the bureaus stay compliant.

Step 1: Conducting a Professional-Grade Credit Audit

You can't fix what you haven't identified. Start by pulling your reports from Equifax, Experian, and TransUnion. While you can access these reports through various services, many beginners find that the most damaging errors are buried in the "personal information" section. Look for mismatched addresses, misspelled names, or incorrect employment history. These seemingly small discrepancies can be used by bureaus to link you to accounts that aren't yours or suggest a lack of financial stability to lenders. A credit audit is the systematic identification of data points that violate reporting standards. This forensic look at your file is the foundation of everything that follows.

Step 2: Drafting and Mailing Legally Compliant Disputes

When you move to the dispute phase, leave the emotional pleas behind. The bureaus don't care about your personal hardships; they only care about whether the data is legally compliant. Your letters must use specific, factual language that points to the exact reporting violation. This is where most people fail. They send generic letters that the bureau's automated systems flag as frivolous. Why do these rejections happen? Usually, it's because the letter lacks the technical specifics required to trigger a mandatory investigation under the FCRA. The bureau's AI looks for specific data markers, and if it doesn't find them, your letter is discarded.

While digital tools make drafting easier, physical mailing via certified mail remains the gold standard. It provides a timestamped paper trail that prevents bureaus from claiming they never received your request. If you're overwhelmed by the paperwork, using an automated credit repair assistant can ensure every letter meets these rigorous standards without the manual stress of typing and mailing dozens of documents yourself.

Step 3: Monitoring and Re-Auditing

Persistence is the final component. Once you mail your disputes, the bureaus have 30 days to respond. If they verify the item, your next step isn't to give up; it's to re-audit. You need to look for new inconsistencies in their verification process. As you rebuild your credit, this cycle of monitoring and re-auditing ensures that your report remains a true reflection of your financial behavior. It's a continuous loop of detection and correction that eventually leads to a clean, accurate profile.

Manual DIY vs. AI-Powered Software: A Comparison for Beginners

Manual credit repair for beginners often starts with a stack of paper and a sense of dread. You have three paths: pay an expensive agency, do it all by hand, or use AI-powered software. Traditional credit repair companies typically charge significant monthly fees for work you could technically do yourself, but they often leave you in the dark about the actual status of your disputes. On the other end, manual DIY feels free until you account for the hours lost. AI-powered software bridges this gap. It provides the professional precision of an agency with the cost-effectiveness and control of a DIY approach, making it the most efficient form of credit repair for beginners in 2026.

Think about the time investment. A manual audit of three credit reports can take ten hours of meticulous reading. You have to cross-reference every date, balance, and account number across three different formats. An AI Credit Specialist like Mo can perform this same analysis in minutes. It doesn't get tired. It doesn't miss a transposed digit in a Metro 2 data string. This accuracy is your greatest leverage. By keeping the process in-house, you also ensure your sensitive data isn't sitting on a third-party agency's server. You maintain total control.

Why Beginners Are Switching to Self-Service Platforms

The "Self-Service Credit Repair Platform" has emerged as the preferred choice for those who value autonomy. These tools don't just draft letters; they analyze data patterns automatically to find violations that are invisible to the naked eye. Seeing your progress in a digital dashboard provides a psychological win that a folder full of paper receipts simply cannot match. You become the protagonist in your own financial recovery. It's about having high-tech equipment that lets you do the work yourself without the traditional middlemen.

The Hidden Costs of Manual DIY

Don't be fooled by the "free" label of manual repair. When you send 20 or more letters via certified mail, the costs for stamps, ink, and postal fees add up quickly. There is also a massive opportunity cost. Do you want to spend your weekends researching obscure legal codes? One wrong word in a manual letter can lead to a "verified" status that is much harder to challenge later. Precision isn't just about speed; it's about protecting your rights from the first click. Manual errors can reset the 30-day clock, costing you months of progress. To succeed, you need to weigh these factors:

- Cost: Software subscriptions are often 70% cheaper than full-service agencies.

- Time: AI reduces paperwork from hours to minutes.

- Accuracy: Automated engines detect technical Metro 2 errors that humans overlook.

- Control: You decide which items to challenge and when.

The Metro 2 Standard: The Beginner’s Secret Weapon

Most guides on credit repair for beginners stop at basic letter writing. They don't tell you about the language the bureaus actually speak. Metro 2 is the universal electronic format used by creditors to send your information to Equifax, Experian, and TransUnion. It isn't a narrative or a story. It's a rigid series of data fields. When you understand this, you stop making emotional pleas and start demanding technical compliance. Banks and bureaus often ignore standard disputes because they are easy to "auto-verify" through their e-OSCAR system. However, they can't easily dismiss a Metro 2 audit. This method forces them to look at specific data fields rather than the general history of the debt. If the data doesn't align with strict Metro 2 guidelines, the bureau is legally obligated to correct or remove it. This is how you transition from basic efforts to expert-level results.

How a Metro 2 Credit Dispute Tool Finds Hidden Flaws

Standard templates are blind to the technical errors that actually get results. Collection agencies often have compliance gaps where they fail to report required fields correctly, such as the Original Creditor or the Account Status. A Metro 2 audit scans 40+ data fields per account to ensure every character reported by the creditor is legally compliant. While a human eye might miss a transposed digit in a date field, an audit engine identifies these discrepancies instantly. This level of precision is what makes credit repair for beginners effective in a system designed to favor the bureaus.

Automating Compliance with the Metro 2 Audit Engine

There's a significant difference between a factual dispute and a Metro 2 compliance dispute. A factual dispute says, "This isn't mine." A compliance dispute says, "You reported this in a way that violates industry standards." The latter is much harder for bureaus to auto-verify. Their e-OSCAR system is programmed to handle simple claims, but it struggles when faced with specific reporting logic errors. By using an automated engine, you identify unverifiable items based on this logic rather than just guessing. You can use the Metro 2 Audit Engine to find exactly what the bureaus are hiding in your report and generate letters that demand a real investigation.

Getting Started: How to Use CreditVault.io to Repair Your Own Credit

You've learned the rules of the data accuracy battle. Now it's time to step into the arena with the right equipment. CreditVault.io isn't a traditional agency that keeps you in the dark; it's a high-tech toolkit designed for absolute autonomy. By using these tools, you bypass the high-cost barriers of middlemen and take direct control of your financial standing. This is the most efficient path for credit repair for beginners because it replaces guesswork with logic and manual labor with automation.

At the center of this experience is Mo, your personal AI Credit Specialist. Mo provides 24/7 guidance, acting as a digital mentor that never sleeps. If you're confused by a specific line item or a bureau's response, Mo is there to provide immediate clarity. This removes the fear of doing it wrong. You aren't alone in the process, yet you remain the one in the driver's seat. Mo works in tandem with the CreditVault.io Metro 2 Audit Engine to scan your reports for the compliance gaps we discussed earlier. It replaces hours of tedious, error-prone manual reading with a technical sweep that identifies every disputable data point in seconds.

Your First 72 Hours on CreditVault.io

The transition from feeling stuck to taking action happens quickly. Once you set up your account and securely import your 3-bureau reports, the system begins its work. Within your first few days, you can complete the following steps:

- Import and Sync: Connect your data from Equifax, Experian, and TransUnion to see your entire profile in one dashboard.

- Run the AI Audit: The engine flags "easy wins" and technical Metro 2 violations that are ripe for challenge.

- Generate Letters: Use Automated Dispute Letter Generation to create legally compliant documents in under 15 minutes.

Once your letters are ready, you have a choice. You can download and mail them yourself via certified mail to maintain your own physical paper trail. If you prefer to save time, you can utilize the concierge mailing service to handle the logistics. Both options ensure your disputes are professional, precise, and impossible for bureaus to ignore.

Empowerment Through Technology

Traditional credit repair for beginners often feels like an endless subscription trap. CreditVault.io changes that by offering flexible Weekly or Monthly Subscription Plans. You pay for the time you need, not for a permanent seat at the table. This transparency is part of our commitment to your autonomy. You get the high-tech equipment of a professional firm without the corporate overhead or opaque processes. It's time to stop being a passive observer of your credit report and start being an active participant in your financial future. Start your AI-powered credit audit today with CreditVault.io.

Reclaim Your Financial Standing Today

The credit reporting system often feels like it's designed to keep you stuck. You've seen that credit repair for beginners is actually a data accuracy battle where technical precision is your greatest weapon. By shifting from emotional pleas to rigorous Metro 2 audits, you force the bureaus to respect your legal rights under the Fair Credit Reporting Act. You don't have to spend your weekends researching legal codes or managing stacks of certified mail receipts. Technology has removed those barriers, allowing you to focus on the results rather than the paperwork.

It's time to move from being a passive observer to an active participant in your financial future. You now have the high-tech equipment to handle your own affairs with professional-grade accuracy. Join CreditVault and let Mo, our AI Credit Genius, audit your report for free. Our platform is powered by Metro 2 Audit technology and AI-driven dispute generation to ensure your data is reported correctly. If you're short on time, our concierge mailing service is available to handle the logistics for you. You have the leverage now. Take the first step toward the freedom and peace of mind you deserve.

Frequently Asked Questions

Is credit repair legal for beginners to do themselves?

Yes, it's 100% legal to manage your own credit repair. The Fair Credit Reporting Act (FCRA) specifically empowers you to challenge any information on your report that you believe is inaccurate or unverifiable. You don't need a lawyer or a professional agency to exercise these rights. Taking a DIY approach to credit repair for beginners is often the most effective way to ensure your data is handled with the care it deserves.

How long does it take to see results with credit repair software?

You should typically expect a response within 30 to 45 days after a bureau receives your dispute. Federal law requires credit bureaus to investigate and respond to your claims within a 30-day window. While some users see corrections in the first round, others may require multiple rounds of auditing and disputing to resolve complex reporting errors. Persistence is the key to seeing long-term results as you navigate this cycle of data correction.

What is the difference between a credit repair agency and a self-service platform?

A credit repair agency acts as a middleman, often charging high monthly fees to send letters on your behalf. In contrast, a self-service platform like CreditVault provides you with high-tech equipment to do the work yourself. This model gives you total transparency and control over your data. You avoid the "black box" feel of traditional services while leveraging professional-grade AI to detect errors that humans often miss during a manual audit.

Can AI really help me remove late payments or repossessions?

AI helps by identifying technical reporting violations that make a late payment or repossession unverifiable. It doesn't "delete the truth," but it scans over 40 data fields to find compliance gaps in how the creditor reported the event. If the bureau or creditor cannot prove the accuracy of every single data point according to Metro 2 standards, they are legally required to remove the entire negative item from your report.

What happens if a credit bureau ignores my dispute letter?

If a bureau fails to respond within 30 days, they are in violation of the FCRA and must remove the disputed item. You should always send your letters via certified mail to establish a timestamped paper trail. If they ignore your request or send a generic "stall letter," you can use your evidence to escalate the dispute. Our platform helps you track these timelines so you know exactly when a bureau has missed their legal deadline.

Do I need to pay for my credit reports separately when using CreditVault?

CreditVault integrates with third-party providers to pull your 3-bureau reports directly into the dashboard. While the software provides the audit engine and AI specialist, you'll need an active credit monitoring account to supply the data. This ensures you're working with the most current information available from Equifax, Experian, and TransUnion. It eliminates the manual stress of uploading paper documents and ensures your credit repair for beginners journey starts with accurate data.

Is my data secure when using an AI credit repair tool?

Security is a core pillar of our technology. We use bank-level encryption and follow strict professional standards to ensure your sensitive financial data remains protected. Unlike traditional agencies where multiple employees might view your file, our automated system processes your data objectively. You maintain autonomy over your information while leveraging a silent partner that works securely in the background to provide you with the necessary leverage.

Can I cancel my credit repair subscription once my score improves?

Yes, you have the total freedom to cancel your subscription at any time. We offer Weekly and Monthly Subscription Plans because we believe you should only pay for the time you actually need. Once your data is reported accurately and you've reached your financial goals, you can stop the service without any long-term contracts or hidden cancellation fees. It's about giving you the leverage to handle your own affairs on your own terms.